Payroll Country Blog

Payroll Country Blog

Your constant source for helpful, useful, and entertaining content about payroll, human resources or anything else that will help you manage your workforce.

Video Series

Video Series

Latest Episode

Conversations with experts in a wide range of HR/HCM topics, for the benefit of anyone whose job it is to manage a workforce or take care of people.

Ashley Explains...

Our Implementation Manager Ashley Hamilton gives you the facts about tax, labor laws, and a whole lot more.

Latest Episode

Our very own Jen Strait and Emily Martin from Ally HR Partners tackle common HR issues and provide practical advice to help you manage your workforce more effectively!

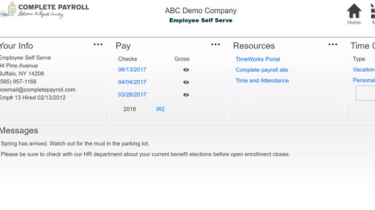

Demo Video Library

Demo Video Library

Featured Demo

Welcome to our comprehensive - yet growing - library of instructional how-to videos that focus on a variety of functions across our software platforms. Scroll down and filter by category or use the search bar to find exactly what you're looking for.

Resource Library

Resource Library

Featured Resource

A robust library of guides, kits and tools designed to educate and support anyone responsible for payroll, HR or managing a workforce of people.

Employer Guides

Employer Guides

An extensive and ever-growing library of super handy employer guides on everything from human resource topics, important Labor Law updates, how to approach payroll for your company's industry, and much more.

Software Downloads

Software Downloads

Quickly reference and download software platforms, installation guides, middleware and other critical files you may need as a client to properly process critical payroll and HR functions with Complete Payroll.

What is Payroll Country?

What is Payroll Country?

What is Payroll Country?

In Payroll Country, people come first, manners aren't optional and a job isn't done until it is. Sure, we're headquartered in a small, rural town. But Payroll Country isn't just where we're from. It's our philosophy of how business should be conducted. Welcome!

Careers

Careers

Careers in Payroll Country

It's not about where we work, it's about how we work. And, more importantly, how we work together.

Client Referral Program

Client Referral Program

Client Referral Program

Earn payroll credit for bringing your colleagues and friends to Payroll Country!

Client Testimonials

Client Testimonials

Featured Testimonial

Check out what some of our most loyal clients have to say about their Payroll Country experience, or leave some kind words about your own.